Most Aussies don’t talk about their credit score until a bank manager politely frowns and says, “Hmm, that might be an issue.” It’s that mysterious three-digit number that seems to decide your financial future—whether you can buy your first home, get a car loan, or just apply for a new credit card.

The thing is, your credit score isn’t some judgment on your moral character. It’s simply a measure of how reliable you look to lenders. Still, plenty of Australians have no clue what their number is, or worse—how to fix it if it’s bad.

This article breaks down everything about Credit Score Australia: what it means, how it’s calculated, how lenders use it, and practical steps to improve yours. And no, it doesn’t involve burning sage or bribing your bank manager with Tim Tams.

Snapshot Summary: Credit Scores at a Glance

For the impatient reader, here’s the cheat sheet:

-

Credit scores in Australia usually range from 0–1200 (depending on the bureau).

-

Good scores = cheaper loans. Bad scores = expensive loans, or flat-out rejection.

-

Your score is influenced by things like repayment history, credit card usage, and how often you apply for credit.

-

You can check your credit report for free every 3 months.

-

Fixing a bad credit score takes time but is very possible with consistent habits.

👉 Want the full story (and a few laughs)? Keep reading.

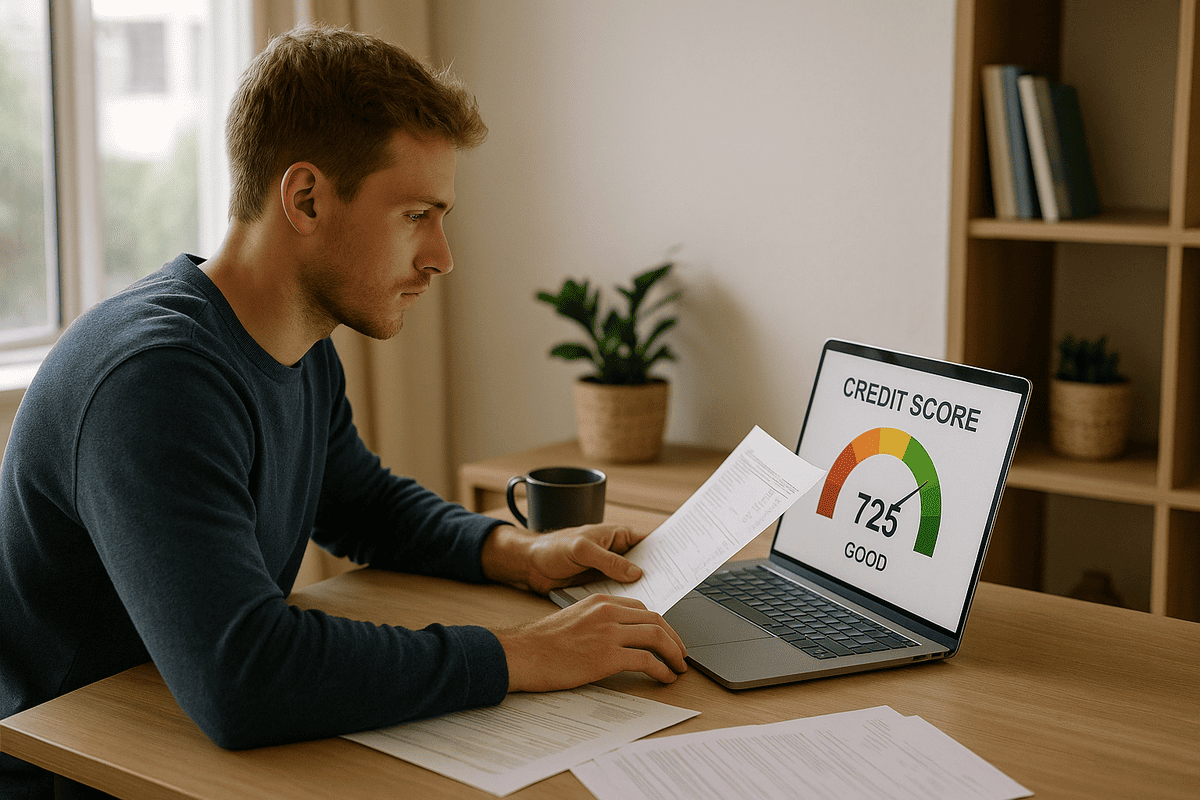

What Is a Credit Score in Australia?

A credit score is basically your financial reputation boiled down into a number. Banks, lenders, and even some landlords use it to decide if they can trust you.

-

Range: In Australia, scores usually go from 0 to 1000 or 1200, depending on the reporting agency (Equifax, Experian, or illion).

-

Categories:

-

Excellent: 800–1200

-

Very Good: 700–799

-

Good: 600–699

-

Average: 500–599

-

Below Average: under 500

-

Did You Know?

An “average” score doesn’t mean you’re doomed. It just means lenders might offer you higher interest rates. Translation: you pay more for borrowing the same money.

How Is Your Credit Score Calculated?

It’s not random, although it might feel that way. The main factors are:

-

Repayment history (35%): Late or missed payments are a red flag.

-

Credit enquiries (20%): Every time you apply for credit, it’s recorded. Too many = desperate vibes.

-

Credit usage (20%): Maxing out your card regularly isn’t a good look.

-

Type and length of credit (15%): A long, stable credit history is better than hopping around.

-

Defaults or bankruptcies (10%): These hit your score hard and stick around for years.

Pro Tip: Even if you pay a loan late by just a few days, it can be marked against you. Banks are not forgiving creatures.

Why Does Your Credit Score Matter in Australia?

Because it literally decides how much your debt costs you.

-

Home loans: A strong score can save you thousands in interest over the life of a mortgage.

-

Credit cards: Better deals, higher limits, and lower rates are all perks of a good score.

-

Car loans & personal loans: Bad scores = fewer options and higher repayments.

-

Even utilities: Some providers check your score before approving electricity or phone accounts.

Better Sleep at Night: How to Check Your Score

Australians can check their credit report for free every 3 months.

-

Agencies: Equifax, Experian, illion.

-

What you’ll see: Your score, repayment history, open accounts, and any defaults.

-

Tip: Check for errors. Mistakes happen, and fixing them can instantly improve your score.

How to Improve Your Credit Score in Australia

1. Pay On Time, Every Time

Even one late payment can ding your score.

Pro Tip: Set up automatic payments. Let tech save you from yourself.

2. Limit Credit Applications

Every application is recorded. Multiple applications in a short time scream “financial trouble.”

3. Keep Old Accounts Open

Longer credit histories look better. Don’t close your oldest credit card just because you don’t use it much.

4. Use Less of Your Credit Limit

If your limit is $10,000, don’t consistently max it out. Aim to use less than 30% if you can.

5. Deal With Defaults ASAP

If you’ve defaulted, paying it off is better than leaving it. The mark stays, but lenders prefer settled accounts.

Quick Guide: When Your Score Needs a Rescue

Situation: You applied for a home loan and got rejected because of your credit score. Panic sets in.

Common Challenges:

-

Do you have multiple missed payments dragging you down?

-

Have you applied for five credit cards in the past year?

-

Is your credit report littered with errors you never knew about?

How to Solve It:

-

Step 1: Review Your Report. Highlight any mistakes and dispute them.

-

Step 2: Automate Payments. Remove human error from the equation.

-

Step 3: Pay Down Debt. Focus on high-interest accounts first.

-

Step 4: Stop Applying. Give your credit file a rest for 6–12 months.

Why It Works:

Consistency and time heal your credit score. No magic trick, just habits that lenders love.

Interactive Quiz: How Credit-Savvy Are You?

-

How often do you check your credit score?

-

A) Never

-

B) Once a year or so

-

C) Every few months

-

-

How do you handle your bills?

-

A) Usually pay late (oops)

-

B) Pay on time most of the time

-

C) Everything is on auto-pay

-

-

How many times have you applied for credit in the past year?

-

A) More than 5

-

B) 2–3

-

C) None

-

Results:

-

Mostly A’s: Your score is crying. Time for action.

-

Mostly B’s: You’re doing okay, but there’s room to improve.

-

Mostly C’s: You’re the kind of borrower banks dream about.

Expert Insight

“Your credit score isn’t permanent—it’s like a school report card. Good habits raise it, bad habits drop it.” – Australian Finance Research Centre

FAQs About Credit Score Australia

Q1: Does checking my score lower it?

No. Only applications for credit (loans, cards) impact your score.

Q2: How long do defaults stay on my report?

Usually 5 years, even if you pay them off.

Q3: Can a bad score stop me renting a house?

Some landlords and agents do check reports, especially for high-demand rentals.

Q4: What’s a “good” score in Australia?

Generally 600+ is considered good, but lenders have their own thresholds.

Q5: How long does it take to fix a score?

Depends on the damage. Minor improvements show in 3–6 months; bigger fixes take years.

Conclusion

Your credit score in Australia is more than just a number—it’s your financial reputation. It affects whether you get approved for loans, how much interest you’ll pay, and even whether you can sign up for a phone plan without hassle.

The good news? It’s not set in stone. By paying on time, limiting applications, keeping old accounts open, and tackling debt, you can steadily improve your score. The sooner you start, the sooner you’ll see results—and the more money you’ll save.

Disclaimer

This article provides general information only. It is not financial advice. For personalised guidance on improving your credit score or managing debt, speak with a licensed financial advisor or credit professional in Australia.